Conventional mortgages are the most popular form of home financing for buyers in the United States. However, it may not always be clear how these loans differ from other loans, such as those provided by government agencies. To help you gain a better understanding of conventional loan basics, here is a quick guide with further information:

The best way to qualify for a conventional loan

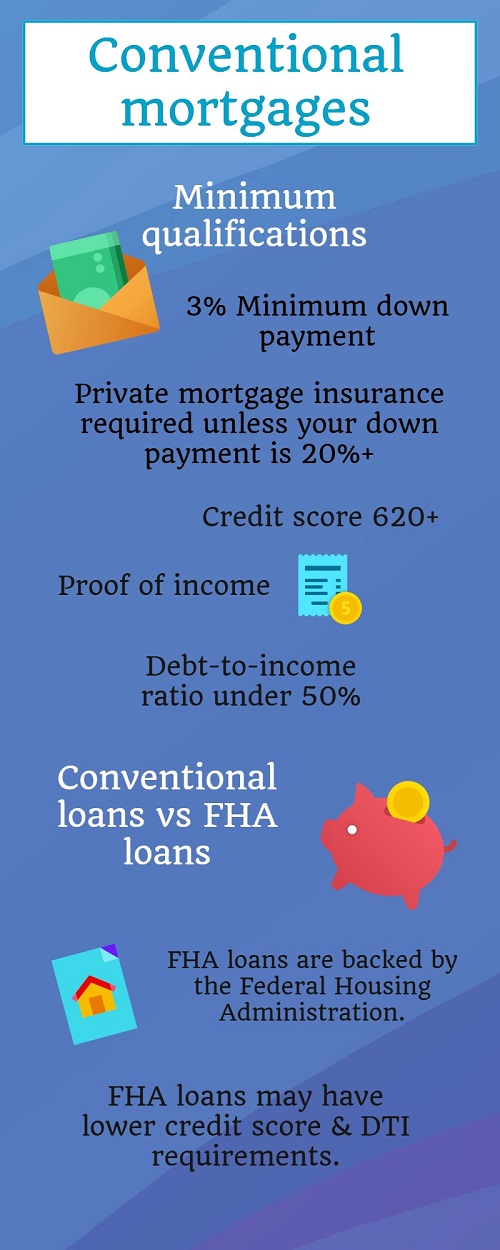

When obtaining conventional financing, your lender will examine your financial situation. The loan officer may request information including your credit score, income statements and debt to income ratios.

A down payment is required for conventional loans. Each lender has different minimum requirements, but the larger the down payment, the less money you’ll have to pay back over time.

Minimum required down payments

Many believe a 20% down payment is required for conventional loans, but the minimum requirement is typically much lower. You can find mortgages with minimum down payment requirements anywhere from 3% to 20% of the overall purchase price.

Your choice of down payment amount can affect the terms of your mortgage, like interest rate or the need for private mortgage insurance.

Conventional loan vs a government loan

Government-backed home loans have specific features to suit some homebuyers.

The Federal Housing Administration (FHA) is a government institution offering home loans for buyers who meet certain qualifications. Government-backed loans have advantages for those with bad credit or other financial roadblocks, but require other qualifications for approval.

Interest rates

Conventional mortgages tend to have higher interest rates than FHA loans, although these loans typically require borrowers to pay mortgage-insurance premiums.

Interest rates charged on a conventional mortgage vary by several factors, including the term and amount borrowed. However, interest rates are also subject to change every year based on the overall economy. Many buyers choose to wait for a period when interest rates are lower to apply for a mortgage, regardless of the loan type.

Ultimately, your choice of loan will depend on your personal circumstances. The more you know about different types of mortgage, the better equipped you’ll be for your journey into thefinancial real estate marketplace.

About the Author

Amie Lindwall-Belile

As your real estate professional, Amie has an extensive knowledge of the local real estate market to meet your needs. Born and raised in Fairfield County she understands the true value of this area. If your money’s involved, then the stakes are high. You can have confidence that Amie will get the job done. Licensed in 2004, she won her office’s Rookie of the Year award. Since then, she has been recognized as a multi-million dollar producer, an Honor Society member, Agent of the Month on numerous occasions and has received various other awards for her successes.

Having graduated from Southern Connecticut State University with a B.S. in Communications focusing on technology, she is able to provide her clients with the most comprehensive cutting edge services and tools. She is the co-founder of an organization close to her heart, The Dennis Lindwall Foundation, running annual events to raise money for pediatric cancer related causes. Over the years, the Dennis Lindwall Foundation has donated more than $100,000 to these charities.

Whether you are buying or selling a home in Fairfield County, you can rest assured that she will work very hard for you. With Amie, you will get the professional yet personalized care that you deserve. Take the first step into this exciting process, with Amie Lindwall-Belile.